How do payment aggregators work, and why are they needed

Publication date: 2025-11-03

Modern e-commerce is impossible without instant and secure online payments. That's why payment aggregators — technological services that integrate various payment methods into a single system — are playing an increasingly important role in Kazakhstan. They help online stores, services, and mobile apps accept payments from customers via cards, e-wallets, mobile operators, and other channels, without having to sign separate agreements with each bank. For businesses, this isn't just a convenience; it's a strategic necessity: aggregators enable payments to be fast, secure, and accessible to customers across the country. Let's take a closer look at how payment aggregators work, what tasks they solve, how they ensure security, and what to consider when choosing a service in Kazakhstan.

What is a payment aggregator?

A payment aggregator is a financial service that acts as an intermediary between a seller and various online payment systems. Simply put, a payment aggregator allows businesses to accept electronic payments from customers through a single platform. Unlike direct bank acquiring (which only accepts card payments), an aggregator supports multiple payment methods, including bank cards (Visa, MasterCard, etc.), e-wallets, online banking, mobile phone balance payments, Apple Pay/Google Pay, and even cryptocurrency with some providers. All these methods are combined in one solution, which greatly simplifies the acceptance of online payments for the seller.Payment aggregators' activities are regulated by financial legislation. Experts define an aggregator as a legal entity engaged by an operating bank to accept electronic payments for organizations, individual entrepreneurs, notaries, the self-employed, and other recipients. Essentially, an aggregator acts as a bank agent, complying with established requirements but handling the technical side of the process. This service is aimed specifically at businesses: companies, sole proprietors, and private practitioners. Direct connection to an aggregator for individuals (i.e., without business registration) is usually unavailable, as most services require the client to be a sole proprietor or a legal entity. There are exceptions: some providers work with the self-employed and certain categories of individuals, offering payment acceptance under special conditions, but in general, payment aggregators are designed to serve entrepreneurs.

It's worth noting the difference between an aggregator and traditional online acquiring. While bank acquiring supports only card payments and often requires a separate agreement with each bank or payment system, an aggregator offers broader functionality and a simpler setup. There's no need to integrate each payment method separately or open multiple accounts with different banks — a single agreement with an aggregator is enough to enable dozens of payment methods on your website. This saves business time and resources, allowing you to launch online sales faster.

How a payment aggregator works with businesses

To start working with a payment aggregator, an entrepreneur must sign an agreement with the chosen service. Typically, connection is done online: simply register on the aggregator's official website and provide the required documents for verification. The provider will verify the legality and reliability of your business (all aggregators have similar requirements: the company must conduct legal activities, and the online store must contain all necessary information about products, seller details, return policy, etc.). Once your application is approved, you will gain access to your personal account and the tools to integrate the aggregator into your website.Aggregator fees are typically charged either as a commission on each transaction or as a subscription fee (or a combination of both). In practice, most aggregators charge a commission as a percentage of the payment amount, without a monthly fee. The commission typically ranges from 2-5% (often around ~3% per payment, and in some cases up to 5% depending on the payment method). For example, some services may only earn money from commissions on successful transactions and do not charge a subscription fee. Other aggregators may offer reduced rates for increased turnover or tailored terms for large clients. It's important for businesses to compare pricing plans from different providers and consider all possible fees (payment acceptance, withdrawals, refunds, etc.).

Once connected to an aggregator, all your customers' payments are processed through its system. Funds from the buyer are credited to the aggregator's transit account and then transferred to your (the seller's) bank account, minus the service's commission. This process usually happens quickly: many aggregators send funds to the seller the next business day after the order is paid. Furthermore, the aggregator doesn't store customer funds long-term, but merely transfers them to your bank. Essentially, the payment aggregator provides the technical infrastructure: it connects the store's website with the necessary payment systems, guarantees the security of the transaction, and then transfers the received funds to your account within the specified timeframe.

An example of an aggregator's operation (payment steps):

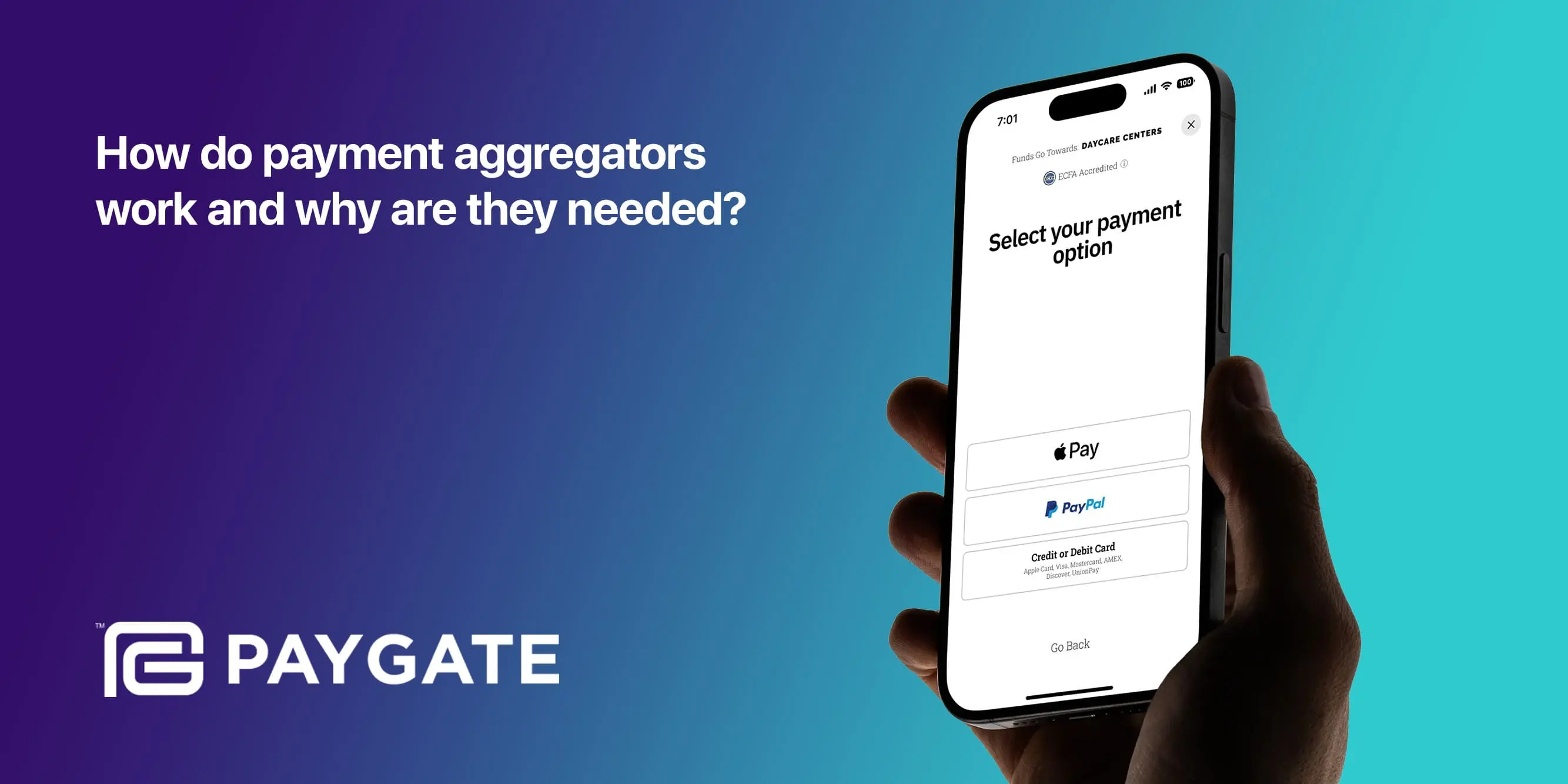

1. The buyer places an order in the online store and proceeds to the payment page.

2. On the payment page, they select a convenient payment method (e.g., card or e-wallet) and enter the required payment details.

3. The aggregator checks the transaction's security (activates anti-fraud protection) and processes the transaction, debiting the specified amount from the buyer's account.

4. After successful payment, the buyer returns to the store's website, and the seller immediately receives a notification about the receipt of funds.

This entire process takes just a few minutes and requires no manual intervention from the business owner – the payment aggregator automates payment acceptance and notifications. Additionally, many aggregators offer modules and APIs for quick integration with a website (on popular CMSs) or even ready-made payment widgets that can be inserted into an online store page without any programming.

The importance of payment aggregators

Today, it's hard to imagine a successful online business without a payment aggregator. If an online store doesn't offer customers a sufficient choice of payment methods, there's a high probability that some customers will turn to competitors. Payment is a key step in the user experience, and it must be as convenient as possible. Payment aggregators solve this problem by providing a single solution for accepting virtually any online payment. Below are the key advantages that make aggregators so essential for businesses:• Single contract and integration.

Connecting to an aggregator saves time and money: instead of signing multiple agreements with banks and payment systems, you sign just one agreement to connect dozens of different payment methods. There's no need to customize your website for each method — the aggregator provides a single API and integration modules for all payments. This is especially important for new online stores with limited resources.

• More payment methods mean more customers.

An aggregator boosts conversion rates and reduces cart abandonment: customers find their preferred payment method immediately on your website and complete their purchase, rather than leaving to look for another store. Support for multiple methods (from cards to mobile payments) expands your audience, allowing you to serve even those who prefer alternative payment methods.

• Transparent reporting and analytics.

High-quality aggregators provide convenient tools for tracking all transactions, generating payment reports, and analyzing sales. All payment information is aggregated in a single personal account, making accounting and monitoring business financial flows much easier.

• Security and anti-fraud.

Modern aggregators provide a high level of data and transaction security. Built-in monitoring systems and anti-fraud filters track suspicious transactions, requesting additional confirmation or blocking fraudulent payments at an early stage. This protects businesses from fraudulent transactions without the need to implement expensive security systems themselves.

• Additional features.

In addition to basic payment acceptance, aggregators often offer additional functionality to support online sales. For example, you can invoice clients via email or messenger (selling without a website), customize the payment page design to match your company style, use recurring payments for subscriptions and regular services, split payments between sellers, and more. These features can prove valuable for your project, increasing the efficiency of your customer service.

Thanks to these advantages, payment aggregators have become an indispensable tool for e-commerce. Their use simplifies life for both entrepreneurs and customers: businesses can more easily organize payment acceptance, and customers can easily and quickly pay for their purchases. Integrating an aggregator is usually straightforward, and the benefits directly translate into increased sales and customer loyalty.

Payment security through aggregators

The security of online payments is vital for any business and its customers, so payment aggregators make it a top priority. Reliable services comply with strict industry data protection standards, the main one being PCI DSS (Payment Card Industry Data Security Standard). This international security standard, developed by the Council of major payment systems (Visa, MasterCard, American Express, etc.), is mandatory for all those processing bank card data.Aggregators undergo regular PCI DSS certification, confirming a high level of cardholder data protection; for example, PayGate LLP has successfully achieved certification for compliance with the Payment Card Industry Data Security Standard (PCI DSS). The audit was conducted by accredited Compliance Control Ltd, a Qualified Security Assessor of the Payment Industry Security Standards Council.

In addition to meeting compliance standards, aggregators employ a range of technical measures to protect each transaction. Data exchange occurs only through secure connections (SSL/TLS), and all confidential information is encrypted and stored on secure servers. To enhance security, many use the "isolated environment" principle: payment information databases do not have direct access to the internet, preventing hacking or data leakage. Data is regularly backed up in case of failures, and access to it is strictly controlled.

Beyond data protection, aggregators implement monitoring and anti-fraud systems. Special algorithms monitor all payments daily, identifying suspicious activity (such as abnormally large or frequent transactions). If a potentially fraudulent transaction is detected, anti-fraud filters are activated: they may require additional verification (for example, entering a 3-D Secure code for a card) or temporarily freeze the transaction. This way, most fraudulent attempts are blocked before funds are debited. Aggregators also protect customers from phishing — all payments are processed on secure payment pages, not on dubious websites.

Thanks to these measures, the level of security when paying through an aggregator is equal to direct payment through the acquiring bank. Buyers can enter their card or e-wallet information without fear of theft, as leading aggregators strictly adhere to personal data protection standards. For businesses, using a certified payment aggregator minimizes the risk of data leakage and gives customers confidence that their money will reach its destination safely.

What should you consider when choosing a payment aggregator in Kazakhstan?

Choosing the right payment aggregator is a crucial step, affecting the convenience of payments and the overall costs of your business. There are many solutions available in Kazakhstan today, so it's worth comparing them based on a number of criteria. Pay attention to rates and fees (payment percentage, setup cost, subscription fees), the payment methods supported by the system, the terms and speed of withdrawals, as well as the level of technical support and additional service features. The provider's reputation is also important: reliable companies with extensive experience and a large customer base typically provide more stable service.Transparent rates and fees

The most important thing to consider when choosing a payment aggregator is the financial terms. The aggregator's commission should be clearly stated in the contract and easy to calculate. Avoid services that charge additional fees for setup, maintenance, or withdrawals. Ideally, the aggregator offers a flexible pricing structure: the higher your turnover, the lower the commission.Supported payment methods

A high-quality aggregator should integrate all popular payment methods, from bank cards (Visa, Mastercard) to mobile payments, Apple Pay, Google Pay, and online banking. The wider the selection, the higher the chance that customers will complete their purchase without interrupting the payment process.Speed of withdrawal and stability of operation

Cash flow predictability is important for any business. A good aggregator should ensure prompt crediting of funds to your account, usually the next business day. Also, pay attention to the service's uninterrupted operation and the availability of 24/7 technical support, especially if you work in e-commerce or mobile services.Local integration and support

Kazakhstan's specific requirements necessitate compliance with national requirements, such as data transfer to tax authorities, integration with domestic banks, and compliance with legislation. Choose platforms that support local tools and offer technical support in Kazakh.Provider reputation and experience

A reliable aggregator is more than just technology; it's a partner you can rely on. The provider should have a solid reputation, a transparent track record, and positive customer reviews. It's important that the company is registered in Kazakhstan and has all the necessary permits and licenses.Conlcusion

Payment aggregators have become a key link in the development of Kazakhstan's digital economy. They not only simplify life for online businesses but also make the market more flexible, transparent, and accessible for small and medium-sized businesses. They allow even small companies to accept payments from anywhere in the country and around the world, while complying with all legal requirements and ensuring a high level of customer data protection.PAYGATE is your technology partner in payment automation for e-commerce and mobile operators. We create solutions that enable businesses to accept and process online payments quickly, securely, and with minimal costs. By partnering with Paygate, you receive a reliable infrastructure adapted to Kazakhstan's realities and international security standards. Entrust your payment processing to us and focus on growing your business.

Subscribe to our Blogs

Receive the most useful information about the global electronic and mobile commerce market in your email